Gaussian Probability Density Function

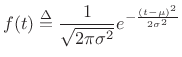

Any non-negative function which integrates to 1 (unit total area) is suitable for use as a probability density function (PDF) (§C.1.3). The most general Gaussian PDF is given by shifts of the normalized Gaussian:

|

(D.28) |

The parameter

Next Section:

Maximum Entropy Property of the Gaussian Distribution

Previous Section:

Why Gaussian?